4 Easy Facts About Mortgage Investment Corporation Described

4 Easy Facts About Mortgage Investment Corporation Described

Blog Article

How Mortgage Investment Corporation can Save You Time, Stress, and Money.

Table of ContentsThe Ultimate Guide To Mortgage Investment CorporationGetting My Mortgage Investment Corporation To WorkGetting The Mortgage Investment Corporation To WorkThe Ultimate Guide To Mortgage Investment CorporationThe smart Trick of Mortgage Investment Corporation That Nobody is Talking About

Does the MICs credit scores board review each mortgage? In the majority of scenarios, mortgage brokers manage MICs. The broker ought to not act as a member of the credit board, as this places him/her in a straight conflict of passion given that brokers usually gain a payment for positioning the home mortgages.Is the MIC levered? Some MICs are levered by a monetary establishment like a legal bank. The monetary establishment will certainly approve certain mortgages possessed by the MIC as safety for a credit line. The M.I.C. will then obtain from their credit line and provide the funds at a greater rate.

This need to offer further examination of each mortgage. 5. Can I have copies of audited financial statements? It is very important that an accountant conversant with MICs prepare these declarations. Audit treatments must make certain rigorous adherence to the plans stated in the information plan. Thank you Mr. Shewan & Mr.

What Does Mortgage Investment Corporation Mean?

Last updated: Nov. 14, 2018 Few financial investments are as useful as a Home loan Investment Corporation (MIC), when it involves returns and tax benefits. Due to their company framework, MICs do not pay revenue tax obligation and are legitimately mandated to disperse all of their revenues to capitalists. On top of that, MIC returns payments are dealt with as passion earnings for tax obligation purposes.

This does not suggest there are not threats, but, normally talking, regardless of what the broader securities market is doing, the Canadian property market, especially major cosmopolitan locations like Toronto, Vancouver, and Montreal does well. A MIC is a firm created under the rules set out in the Earnings Tax Obligation Act, Section 130.1.

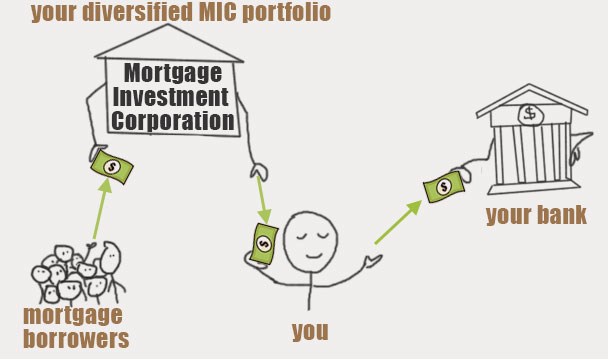

The MIC makes revenue from those home loans on passion charges and basic fees. The actual allure of a Home mortgage Financial Investment Corporation is the return it offers financiers compared to other fixed income investments. You will have no problem locating a GIC that pays 2% for an one-year term, as government bonds are similarly as low.

Not known Details About Mortgage Investment Corporation

A MIC needs to be a Canadian company and it need to spend its funds in mortgages. That claimed, there are times when the MIC finishes up having the mortgaged residential property due to repossession, sale agreement, etc.

A MIC will make interest revenue from home loans and any kind of money the MIC has in the financial institution. As long as 100% of the profits/dividends are provided to investors, the MIC does not pay any earnings tax. Rather than the MIC paying tax obligation on the interest it makes, shareholders are responsible for any kind of tax.

Get This Report about Mortgage Investment Corporation

And Deferred Strategies do not pay any tax on the passion they are approximated to obtain - Mortgage Investment Corporation. That stated, those that hold TFSAs and annuitants of RRSPs or RRIFs might be hit with particular fine tax obligations if the investment in the MIC is considered to be a "forbidden investment" according to Canada's tax obligation code

They will certainly ensure you have actually located a Home mortgage Financial investment Firm with explanation "competent investment" status. If the MIC certifies, maybe very helpful come tax obligation time since the MIC does not pay tax obligation on the passion income and neither does the Deferred Plan. Much more extensively, if the MIC falls short to meet the requirements established out by the Revenue Tax Act, the MICs income will certainly be taxed before it obtains distributed to investors, lowering returns substantially.

It appears both the real estate and supply markets in Canada go to this web-site are at perpetuity highs On the other hand returns on bonds and GICs are still near record lows. Also cash is shedding its appeal because energy and food rates have actually pressed the rising cost of living price to a multi-year high. Which pleads the question: Where can we still locate value? Well I think I have the solution! In May I blogged about checking out home loan investment corporations.

The 2-Minute Rule for Mortgage Investment Corporation

Several difficult working Canadians that intend to purchase a house can not get home mortgages from typical banks since possibly they're self employed, or do not have an established credit report background yet. Or possibly they desire a brief term car loan to develop a huge building or make some restorations. Banks have a tendency to overlook these potential borrowers because self utilized Canadians don't have stable incomes.

Report this page